VAT On Educational Services in the UAE demands precise handling in 2026, especially as the booming education sector—from Dubai’s international schools to Abu Dhabi’s universities—navigates zero-rated tuition alongside 5% VAT on ancillary fees under Federal Decree-Law No. 8/2017 (VAT Law) and FTA Public Clarification VATFDPC002. With registration thresholds steady at AED 375,000 taxable supplies, e-invoicing pilots expanding, and 2026 amendments capping refunds at five years while simplifying reverse charge rules, schools risk AED 500+ penalties per non-compliant invoice if they misclassify supplies.

Understanding VAT On Educational Services Basics

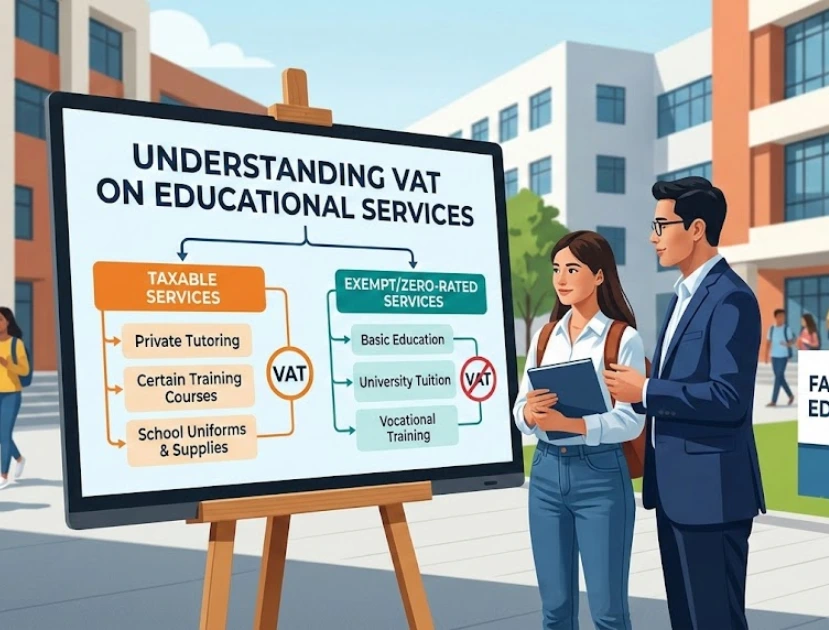

VAT on educational services creates a clear divide between core academic activities (often zero-rated) and supplementary services (standard 5% VAT), designed to support UAE’s Vision 2031 education push while maintaining revenue neutrality. Qualifying educational institutions—government-subsidized nurseries/preschools, KHDA/MoE-licensed K-12 schools, and accredited universities—zero-rate tuition fees leading to recognized qualifications like GCSEs, IB diplomas, or bachelor’s degrees. This means no 5% VAT charged to parents, but full input VAT recovery on related costs.

Non-qualifying services hit standard 5% VAT: Private tutoring, language/conversational classes, hobby courses (art, music unless curriculum-integrated), vocational training without accreditation, and conference/seminar fees. The FTA defines “education” narrowly—recognized curricula delivered by licensed bodies. Mixed bundles complicate matters: A AED 20,000 annual fee package including zero-rated tuition + taxable uniforms/transport requires apportionment by fair value or usage.

2026 brings practical shifts via Decree-Law No. 16/2025: Imported educational technology (e.g., online platforms from abroad) falls under simplified reverse charge—no self-invoicing needed, just proof retention for input claims. The five-year VAT credit refund limit pressures schools to audit 2021+ claims before December 31 expiry. Early compliance prevents cascading penalties amid FTA’s increased education sector audits.

Qualifying vs Non-Qualifying Educational Services

Zero-Rated Educational Services (Article 40, VAT Law): Core tuition at licensed institutions delivering government-recognized qualifications. This covers:

- Nurseries/preschools (MoHES-approved curricula)

- Primary/secondary schools (KHDA/MoE licensed, leading to Tawjeeh/EmSAT/IB)

- Universities (CAA/MoE accredited degrees)

- Bundled exams, graduation ceremonies, and directly supplied textbooks/e-learning materials

- Vocational training with Ministry recognition

Standard-Rated 5% Services:

- Uniforms, school bags, stationery sold separately

- Transportation (school buses, unless curriculum-integrated field trips)

- Boarding/hostel accommodation (treated as residential)

- Cafeteria/canteen food sales

- Extracurricular activities (sports clubs, drama—unless core curriculum)

- Private tutoring, test prep outside accredited programs

- Event fees (parent-teacher meetings if charged, school fairs)

FTA examples clarify: A Dubai British school zero-rates AED 50,000 KG1 tuition but charges 5% VAT (AED 525) on AED 10,500 uniform/transport package. Non-accredited online courses? Full 5% from day one.

VAT Registration Thresholds for Schools

Mandatory registration triggers at AED 375,000 total taxable supplies over 12 rolling months—including zero-rated tuition in the calculation. A growing international school hitting AED 2 million zero-rated fees + AED 200K taxable extras must register immediately. Voluntary registration below threshold unlocks input recovery on furniture, lab equipment, and teacher training—crucial for capital-intensive startups.

Post-registration (3-10 days via EmaraTax), issue tax invoices with TRN for all supplies—even zero-rated ones require “Zero-rated supply” notation. Free zone schools (e.g., Dubai Knowledge Park) follow identical rules but coordinate with corporate tax QFZP status. Deregistration possible if dropping below AED 187,500 (no activity 12 months), but retain 6 months records.

Input VAT Recovery Rules

Zero-rated schools recover 100% input VAT on directly related costs: Textbooks, scientific equipment, online learning platforms (if curriculum-tied), teacher training courses, and facility maintenance for academic use. Partial recovery applies to mixed inputs—school buses (70% zero-rated student transport, 30% taxable field trips = 70% recovery), photocopiers (80% academic printing).

Blocked inputs include staff entertainment, exempt residential dorm supplies, or personal use. Apportionment methods:

- Fair Value: Tuition revenue vs. total (AED 8M zero-rated / AED 10M total = 80% recovery)

- Direct Attribution: Fully academic (lab chemicals = 100%)

- Usage: Metered logs (electricity academic vs. admin)

Notify FTA for method changes; retain 5-year proof. 2026’s five-year refund cap means review 2021 claims now—many schools sit on AED 100K+ unclaimed inputs.

Tax Invoice Requirements for Educational Services

Mandatory Elements (Even Zero-Rated):

- Supplier full TRN (15 digits)

- Invoice date, sequential number

- Parent/student name/address

- Clear description: “Zero-rated Grade 5 tuition Q1 2026” vs. “Standard-rated uniform package”

- VAT rate (0% or 5%), amount

- Total value

E-invoicing (mid-2026 B2B): XML-embedded PDF+A for textbook suppliers. Simplified invoices (<AED 10K retail to parents) allowed but must show TRN. Parents demand compliant bills for their business input claims. Non-compliant? AED 500 per invoice + blocked recoveries.

Apportionment Methods for Mixed Supplies

Schools bundle complexly—tuition (zero-rated) + transport (5%). Methods:

- Fair Value Method: Revenue proportion (90% tuition revenue = 90% zero-rated classification)

- Usage Method: Student hours (80% classroom vs. 20% sports = 80% recovery)

Example Calculation: AED 12M annual revenue (AED 10M tuition zero-rated, AED 1M transport 5%, AED 1M uniforms 5%). Apportionment ratio: 10M/12M = 83%. AED 200K total inputs VAT recovered: AED 166K (83%).

FTA requires annual reviews; changes need approval. Poor apportionment costs schools 2-5% margins annually.

2026 VAT Updates Impacting Schools

Decree-Law No. 16/2025 Key Changes:

- Reverse Charge Simplification: Imported edtech/curricula—no self-invoice needed; report/pay VAT, claim input same return with proofs

- Five-Year Refund Limit: Pre-2021 credits expire Dec 31, 2026—audit now

- E-Invoicing Phase 2: B2B mandatory (textbooks, furniture); schools test XML compliance

- Cumulative Penalties: Late return AED 500 + inaccuracy AED 10K stack

FTA targets education for uniform/transport misclassification audits.

Compliance Checklist for Educational Institutions

Monthly Tasks:

- Track total supplies vs. AED 375K threshold

- Segregate zero/standard revenue in accounting

- Issue TRN-compliant invoices

Quarterly:

- File VAT return (due day 28)

- Reconcile/apportion inputs

- Review e-invoice readiness

Annual:

- Method review notification

- Aged credit claims

- Mock audit

Common VAT Pitfalls in Education Sector

- Over-Zero-Rating: Taxing non-accredited extracurriculars as tuition (FTA reclassifies + back tax)

- Input Overclaim: Recovering VAT on blocked dorm supplies

- Bundling Errors: Hiding taxable transport in tuition fees

- Late Registration: Post-enrollment growth breaches threshold unnoticed

- Poor Apportionment: Static ratios despite shifting student mix

Real cost: AED 25K+ penalties + 2% margin erosion.

Pitfalls Table

| Pitfall | Risk | Fix Strategy |

|---|---|---|

| Zero-rating hobby classes | AED 10K reassessment + interest | KHDA/MoE license verification |

| No TRN on parent bills | Blocked client recoveries | Invoice template audit |

| Static apportionment | 20% input overclaim denial | Quarterly usage logs |

| Bundled taxable extras | Full reclassification | Separate line items |

| Late threshold breach | AED 10K registration fine | Monthly turnover tracking |

Penalties for VAT Non-Compliance

Administrative Fines:

- Late VAT return: AED 500

- Incorrect return: AED 10K

- Invalid invoice: AED 500 each

- E-invoicing non-compliance: AED 20K/month

Tax-Geared: 100-200% of underpaid VAT for evasion. Interest: 14% annual on late payments. Voluntary Disclosure pre-audit reduces to 1% monthly—schools use for apportionment fixes.

Expert Assistance Options

Tax consultants provide:

- Registration + TRN setup (AED 3K-5K)

- Apportionment studies (AED 10K)

- Mock audits + VD (AED 15K)

- E-invoicing implementation (AED 20K+)

ROI: AED 50K+ annual savings via proper recoveries.

Case Studies: Schools Getting VAT Right

Dubai International School: Recovered AED 250K inputs via usage-based bus apportionment (75% recovery vs. prior 50%).

Abu Dhabi University: Zero-rated imported LMS platform correctly, saving AED 75K VAT annually.

Sharjah Nursery Chain: Voluntary registration unlocked AED 40K textbook recoveries despite sub-threshold.

Master VAT On Educational Services for UAE School Success

Navigating VAT on educational services in the UAE positions schools, universities, and training centers for compliant growth in 2026, balancing zero-rated tuition benefits with 5% charges on uniforms, transport, and extras while maximizing input recoveries through smart apportionment and timely filings. From registration thresholds to e-invoicing readiness and avoiding AED 500+ penalties per invoice, this complete guide equips institutions to turn complex VAT rules into operational advantages rather than costly pitfalls.

Stay ahead of VAT on educational services updates, FTA clarifications, and 2026 compliance shifts with Tax News—your essential resource for UAE tax guides, school-specific checklists, and real-time regulatory alerts. For personalized expert assistance with VAT registration, apportionment studies, mock audits, or full compliance outsourcing, connect with My Taxman at mytaxman.ae.. As Dubai’s best tax consultants specializing in education, we’re ready to book your tailored VAT strategy session today.

Frequently Asked Questions

Is VAT applicable on education in the UAE?

Zero-rated educational services carry a 0% VAT rate. This allows institutions to skip charging VAT to students while still reclaiming (recovering) VAT paid on their own business expenses.

Is VAT on education legal?

Generally the supply of education is VAT-exempt. This has meant that historically private schools have not charged VAT on their fees. In its 2024 general election manifesto the Labour Party stated that in government it would remove the VAT exemption that applies to private school fees.

Which services are exempted from VAT in the UAE?

Here is a concise summary of the UAE VAT list for 2026. Note that “Exempt” and “Zero-rated” are different: Zero-rated businesses can reclaim VAT on expenses, while Exempt businesses cannot.

Is VAT included in school fees?

The supply of educational services by certain institutions such as schools, universities, technikons and colleges is exempt from VAT under section 12(h)(i) of the Value-Added Tax Act 89 of 1991 (the VAT Act).

What is the new VAT rule in UAE 2026?

Effective January 1, 2026, the UAE is implementing major VAT amendments via Federal Decree-Laws No. 16 & 17 of 2025, focusing on administrative simplification and stricter compliance. Key changes include removing self-invoicing for reverse charges, a 5-year limit for tax refunds, and increased FTA authority to deny input tax deductions

Is there VAT on professional services in UAE?

The standard VAT rate in the UAE is 5%, which applies to most goods and services supplied within the UAE. This includes: Retail sales of goods. Professional services.