VAT treatment of free samples and promotional goods in the UAE can catch businesses off guard, turning what seems like a simple marketing gesture into a taxable event. Under UAE VAT law, handing out complimentary items isn’t always “free” from a tax perspective. This guide breaks down the rules, exceptions, documentation and best practices so you stay compliant without derailing your promotions.

Understanding VAT Treatment Of Free Samples

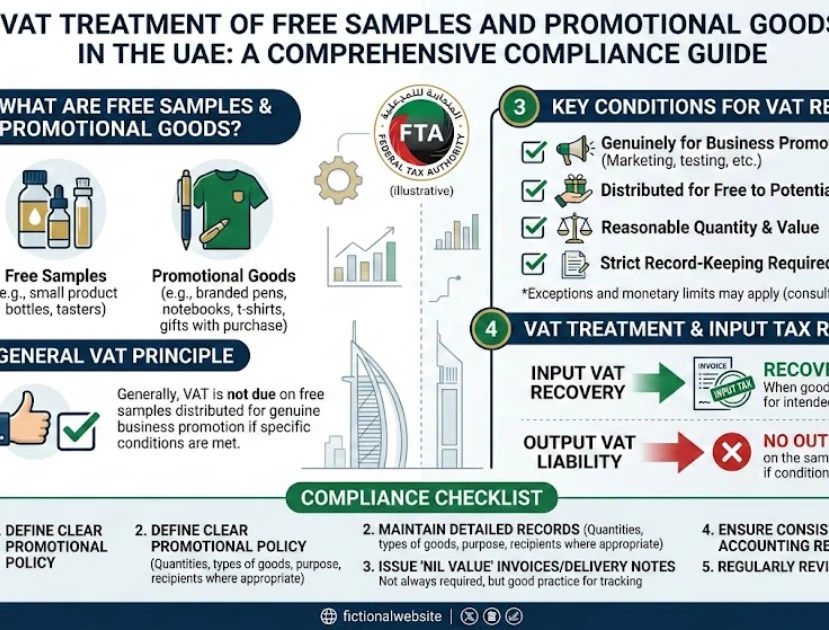

In UAE VAT terms, free samples and promotional goods often qualify as deemed supplies under Article 25 of the Executive Regulations to Federal Decree-Law No. 8 of 2017 on VAT. This means they are treated as taxable supplies, even without payment, requiring you to account for 5% output VAT on their value. The logic? The FTA views these as business activities aimed at generating future sales, so VAT applies to keep the system fair.

Secondary keywords like VAT on free samples, promotional goods VAT UAE and deemed supply VAT come into play here. If you’ve claimed input VAT on the goods’ purchase or production, you generally must charge output VAT on the giveaway value. But there are key exceptions we’ll cover next.

When Free Samples Are Not Taxable

Not every complimentary item triggers VAT treatment. FTA Public Clarification VATP020 and related guidance outline exemptions:

1. No Input VAT Recovered

If you didn’t recover input VAT on the related goods (e.g., exempt purchases or blocked input tax), no output VAT is due. This is common for businesses dealing in zero-rated or exempt items like certain healthcare products.

2. Business Gifts Under AED 200 per Person per Year

Small gifts to employees or clients, valued at AED 200 or less per recipient annually, are disregarded for VAT if they are promotional, advertising or courtesy items. Think branded pens or calendars—practical and low-value.

3. Samples for Testing or Quality Control

True free samples given solely for customer evaluation (not resale) may qualify for relief if documented properly and input VAT was not recovered. However, mass distributions often fail this test.

VAT treatment changes if the free item is part of a bundled sale (e.g., “buy one, get one free”). Here, treat as a discount on the total supply, not a separate deemed supply.

Promotional Goods and “VAT-Free” Offers: FTA Warnings

Many retailers advertise “VAT-free” promotions, but FTA Public Clarification VATP020 calls this misleading. Sellers must charge VAT on promotional goods; absorbing it as a discount is fine commercially, but you can’t opt out of VAT liability. For example:

- Scenario: Sell goods for AED 100 + AED 5 VAT, but promote as “VAT-free AED 100”. You still owe the AED 5 to FTA; it’s effectively a discount.

Tax invoices must comply with Article 59, listing full details even for promotions. Failure risks audits and penalties.

Calculating VAT Value for Deemed Supplies

For VAT treatment where output is due, value the supply at open market value (fair price to an unrelated buyer). Methods:

- Comparable Sales: Use recent prices for identical items.

- Cost Plus Markup: Production cost + reasonable profit margin.

- Discounted Price: If part of a promotion, adjusted sale value.

Document your valuation method consistently to defend during audits.

Documentation and Record-Keeping Requirements

Proper records are your shield. For free samples VAT treatment:

- Internal Records: Recipient details, item description, value, date, purpose (e.g., “promotional sample”).

- No Tax Invoice Needed: But log as deemed supply in VAT return.

- Retention: 5 years minimum (7 for customs-related).

Use ERP systems to flag free issues automatically.

Common Scenarios and VAT Treatment Examples

Scenario 1: Retail Free Sample

Beauty store gives AED 50 lipstick samples (input VAT recovered). VAT Treatment: Deemed supply at AED 50; output VAT AED 2.50.

Scenario 2: Buy-One-Get-One-Free

Sell two shirts AED 200 total (AED 100 each). VAT Treatment: Single supply AED 200 + AED 10 VAT; no separate deemed supply.

Scenario 3: Employee Gift

AED 150 hamper per staff (under AED 200). VAT Treatment: Disregarded, no VAT.

Scenario 4: Client Christmas Hamper AED 300

VAT Treatment: Deemed supply AED 300; output VAT AED 15 (if input recovered).

Impact on VAT Returns and Audits

Deemed supplies appear in Box 1 of your VAT return (taxable supplies). Reconcile with accounts to avoid mismatches. During audits, FTA checks:

Non-compliance risks assessments plus 200% penalties on underdeclared VAT.

Best Practices for Compliant Promotions

- Pre-Approve Promotions: Review VAT impact before launch.

- Track Values: Use inventory systems for sample costing.

- Train Staff: Ensure sales teams log free issues.

- Seek Clarification: Use FTA helpline for edge cases.

- Annual Review: Audit gift/sample spending vs. thresholds.

Recent FTA Updates Affecting VAT Treatment

Cabinet Decision No. 100/2024 amended VAT Executive Regulations effective Nov 2024, clarifying input tax on mixed supplies but not changing core deemed supply rules for promotions. Stay tuned for digital invoicing ties (2026), which may require XML logging for free issues.

Audit Triggers and How to Prepare for FTA Free Sample Reviews

FTA audits often target promotional-heavy sectors like FMCG, retail and hospitality, where free samples represent material VAT exposure. Common triggers include mismatched inventory shrinkage vs. reported deemed supplies, customer complaints about inconsistent pricing, or whistleblower tips on unlogged giveaways. When selected for review, expect FTA to request 5-year records of all promotional activities, sample valuations, input recovery patterns and sales data showing promotion impact. Preparation starts with pre-audit self-assessments: quarterly reviews matching sample logs against VAT returns, testing valuation reasonableness against comparable sales, and verifying employee gift totals stay under thresholds.

Myths and Misconceptions

- Myth: All free samples are VAT-free. Fact: Only if no input recovered.

- Myth: “VAT-free” ads are okay. Fact: Misleading per FTA.

- Myth: No invoice = no VAT. Fact: Deemed supplies still reportable.

Simplifying VAT Treatment Through Tax News and My Taxman

Tax News serves as your reliable partner in navigating the complexities of VAT treatment scenarios like free samples and promotional goods in the UAE. We cut through the technical jargon of FTA public clarifications, Cabinet Decisions and Executive Regulations to deliver straightforward, actionable insights that busy business owners, accountants and finance managers can apply immediately. Whether it’s understanding deemed supply rules, documenting promotional giveaways or avoiding common pitfalls during audits, our regularly updated articles ensure you’re never caught off guard by the latest VAT developments.

My Taxman takes this knowledge one step further with hands-on, personalised VAT advisory services tailored specifically for businesses dealing with promotional activities, retail promotions and marketing giveaways. Our team of UAE VAT specialists conducts thorough audits of your current promotion practices, reviews input VAT recovery patterns and designs compliant processes that minimise tax exposure while maximising marketing impact. From setting up proper documentation templates and ERP flags for deemed supplies to representing clients during FTA queries or assessments, My Taxman ensures your VAT treatment of free samples and promotional goods is not only technically correct but also strategically optimised.